For data-dependent central banks, the next 12 days offer a smorgasbord of indicators. CPI, GDP, jobs numbers, inflation expectation surveys, you name it.

Investors have wagered ungodly sums on the inflation picture improving this summer. This next batch of data is crucial to them being right, and to the lid

For data-dependent central banks, the next 12 days offer a smorgasbord of indicators. CPI, GDP, jobs numbers, inflation expectation surveys, you name it.

Investors have wagered ungodly sums on the inflation picture improving this summer. This next batch of data is crucial to them being right, and to the lid being kept on yields—and mortgage rates.

The marquee number for the BoC is CPI. It drops today, and the consensus calls for 3.4%. That would be down one whole percentage point from April.

If that's what we get, it may be largely attributable to #base effects#. To get a better read of the underlying trend, the BoC will focus on its favoured 3-month core measure instead.

💡

MLN will have full CPI coverage after its 8:30 a.m. release today.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

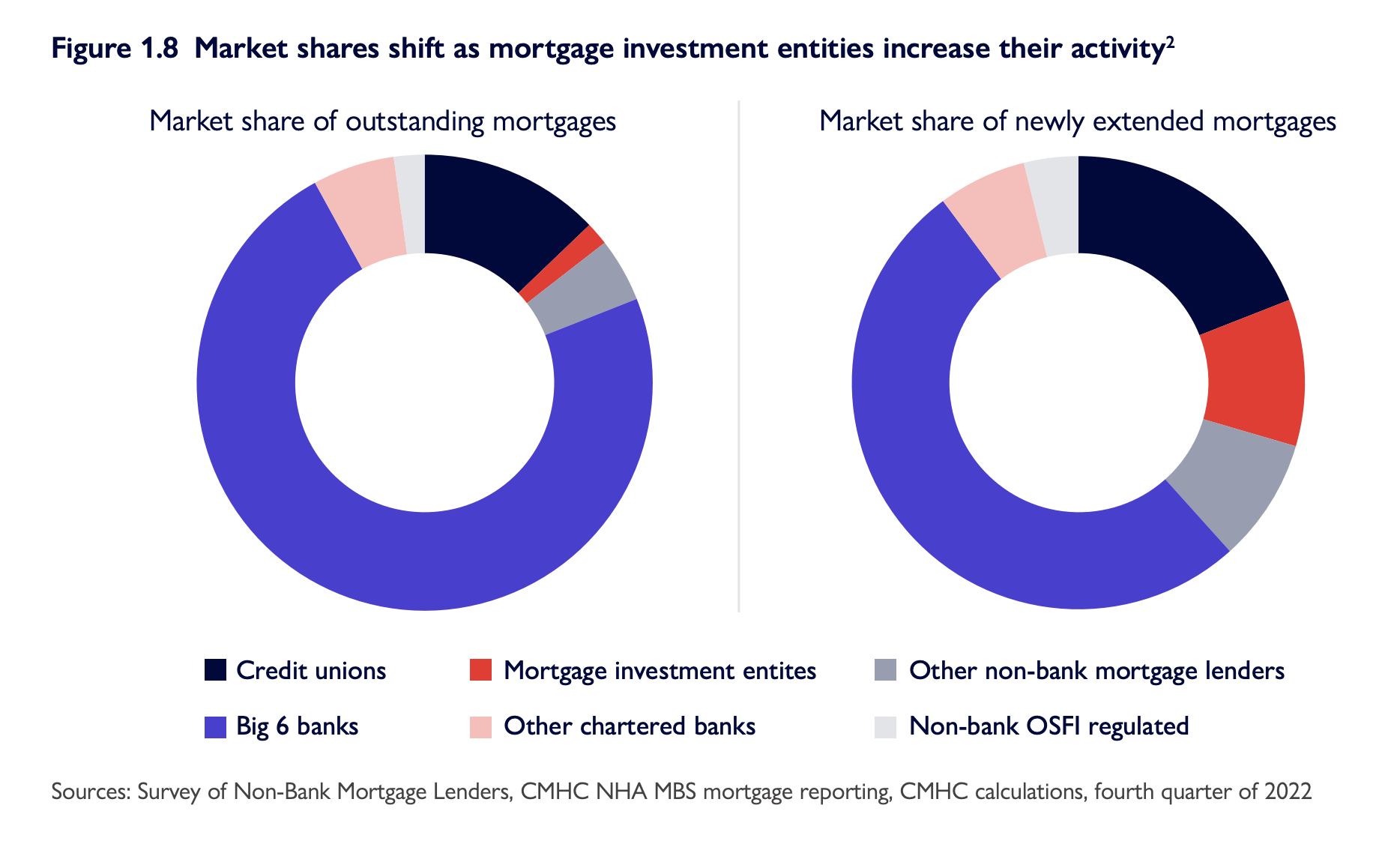

Qualifying for a mortgage takes a lot more strategy than it used to. And banks are no longer the right move for millions of Canadians, as this chart below illustrates.

The share of mortgage business now flowing to credit unions, private/MIC lenders, and other non-banks is remarkable.

Federal policy

Qualifying for a mortgage takes a lot more strategy than it used to. And banks are no longer the right move for millions of Canadians, as this chart below illustrates.

The share of mortgage business now flowing to credit unions, private/MIC lenders, and other non-banks is remarkable.

Federal policy has driven "riskier" borrowers outside the banking system since 2008. But all that risk still exists. It's just distributed differently now.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Few Canadians understand how crucial the Canada Mortgage Bond (CMB) program is to facilitating more mortgage options and lower rates.

Given all the government-imposed costs and limits on the CMB and #NHA MBS# programs since the #GFC# (wow, that's a lot of acronyms for one sentence), we wonder

Few Canadians understand how crucial the Canada Mortgage Bond (CMB) program is to facilitating more mortgage options and lower rates.

Given all the government-imposed costs and limits on the CMB and #NHA MBS# programs since the #GFC# (wow, that's a lot of acronyms for one sentence), we wonder if even housing policymakers fully grasp its importance.

"The only way our small lenders compete is to have an edge on pricing," a major bank aggregator (mortgage investor) told us. "If anything prices outside where big banks price, they don’t have a chance." The government-backed CMB program is a crucial source of this low-cost funding, especially in the mortgage broker channel.

Despite its importance, the government is looking to end the Canada Mortgage Bond (CMB) system as we know it...and replace it with something else.

That "something else" has been a huge question mark because the Department of Finance has released so little information thus far—besides this consultation document.

After reading the document, National Bank Financial (NBF) called the proposal "one of the most material changes ever proposed for Canada’s domestic bond market."

The government's initiative begs all sorts of questions. Among them:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Canada's average home price has rocketed 19% from January's low. Regardless of one's opinion of average prices as a measure, that's monumental.

By June 7, Tiff & Co. at the BoC had seen enough. Their deliberations, published Wednesday, confirmed that resale housing&

Canada's average home price has rocketed 19% from January's low. Regardless of one's opinion of average prices as a measure, that's monumental.

By June 7, Tiff & Co. at the BoC had seen enough. Their deliberations, published Wednesday, confirmed that resale housing's extraordinary "momentum" was a key reason for their un-pausing this month. The BoC remarked that "housing resale prices—which feed into the CPI with a 1-month lag—had increased for three consecutive months."

Meanwhile:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Just as new rate hikes threaten to push more mortgagors over the edge, we got this ominous headline from Reuters last week:

"Canada bank regulator says lenders should urgently tackle risks from mortgage extensions"

This got worrywarts in the housing market all riled up, thinking new regulatory policies

Just as new rate hikes threaten to push more mortgagors over the edge, we got this ominous headline from Reuters last week:

"Canada bank regulator says lenders should urgently tackle risks from mortgage extensions"

This got worrywarts in the housing market all riled up, thinking new regulatory policies might drive borrowers into default. So, we decided to investigate what OSFI was actually proposing.

Here's what Canada's bank regulator told us:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

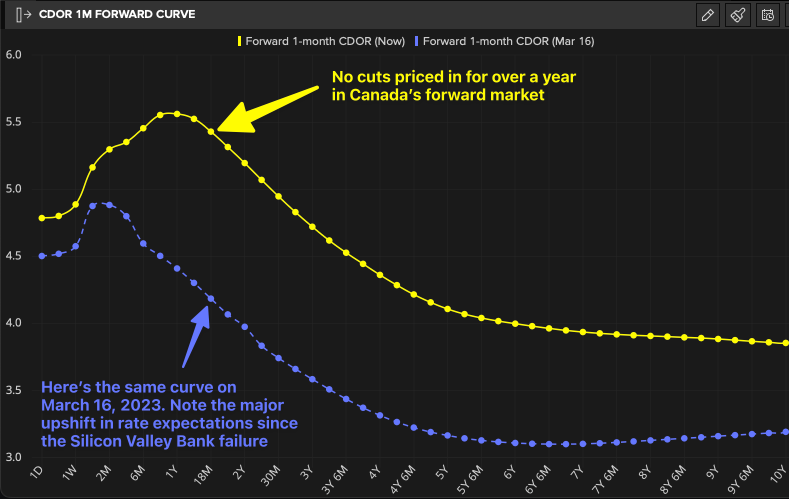

The chart above shows how much Canada's roller coaster rate outlook has changed in just 90 days.

The purple line shows the Bank of Canada cuts that were expected this year, just after the Silicon Valley Bank drama in March.

The yellow line shows where the market now

The chart above shows how much Canada's roller coaster rate outlook has changed in just 90 days.

The purple line shows the Bank of Canada cuts that were expected this year, just after the Silicon Valley Bank drama in March.

The yellow line shows where the market now thinks the BoC is headed, give or take.

We still get cuts either way, barring an external inflationary shock. It's just that now we have to wait longer for them. On top of that, investors now believe the average implied BoC rate over the next five years will be 104 bps higher than they thought in March.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Mortgage originators all feel how tough it is out there. But the latest stats put the challenge in perspective.

"The entire mortgage originations pie has shrunk by 42%," says veteran broker Jim Tourloukis of Advent Mortgage Services, citing first-quarter Equifax data on new mortgage volumes.

And not only

Mortgage originators all feel how tough it is out there. But the latest stats put the challenge in perspective.

"The entire mortgage originations pie has shrunk by 42%," says veteran broker Jim Tourloukis of Advent Mortgage Services, citing first-quarter Equifax data on new mortgage volumes.

And not only is the pie smaller, but brokers are getting a smaller piece. CMHC data shows broker market penetration fell from 51% in 2022 to 43% in January. "I suspect this will be lower in Q2," Tourloukis estimates. "Also, these numbers are worse for uninsurable business."

But wait, there's more. To milk the desert analogy further, not only are brokers getting a smaller piece of a smaller pie, but "the pie doesn't taste as sweet as it used to," he says.

Why?

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

In the last two years, we don't know any mortgage marketer who's made more progress on Google than the financial comparison site, Wowa.ca.

It's climbed the Google ranks and built a 7-figure revenue in just five years. And just last week, it set

In the last two years, we don't know any mortgage marketer who's made more progress on Google than the financial comparison site, Wowa.ca.

It's climbed the Google ranks and built a 7-figure revenue in just five years. And just last week, it set a new personal best of 36,424 visits in one day, breaking its record for paid leads.

They know what they're doing over there, and we can all take something from Wowa's success.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.