💡Also in this edition:

• The latest from RateLand

• The Value Zone (with new fixed-variable research from Desjardins)

• Mortgage Bytes

Toronto-based mortgage broker 8Twelve Mortgage Corporation has just scored a lucrative long-term revenue-sharing pact with NerdWallet (Nasdaq: NRDS).

San Francisco-based NerdWallet is a global financial information juggernaut. In Canada, it competes against Ratehub, Wowa, and countless others to deliver rate comparisons and advice to mortgage consumers. Its gl...

MLN NewsStream

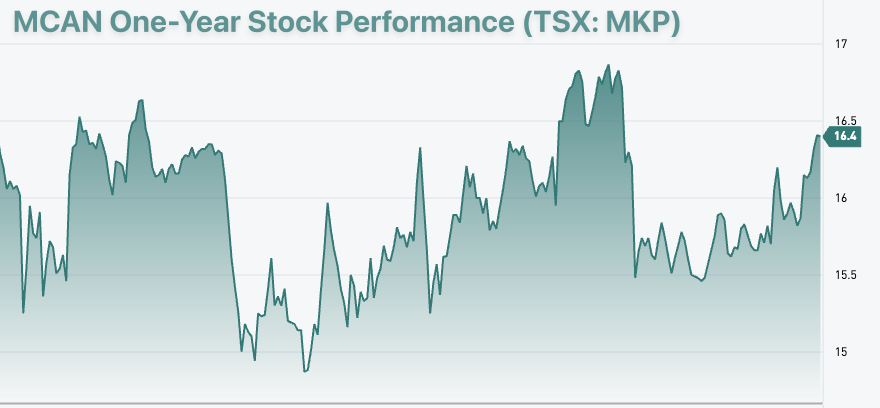

MLN Interviews MCAN: Value Mortgage Leader. Stealth Wealth Builder

When the public thinks about where to get a mortgage, MCAN doesn’t pop up on most radars. However, for status brokers in the know, MCAN is sometimes invaluable for ultra-rate-sensitive insured clients. It also fills some quirky non-prime niches.

And then there's its stock. Investors know MCAN Financial for its irresistible dividend (almost 10%), payout track record and 12.39% ten-year compound annual growth rate. MCAN is also Canada's largest Mortgage Investment Corporation ("MIC") and the only...

CMHC Undercuts Sagen and Canada Guaranty

CMHC has massively undercut private default insurers on 30-year insured amortizations.

Effective August 1, Canada's housing agency will be charging just 20 bps extra for insured first-time buyers who want a 30-year am. That's dialling all the way back to what CMHC charged in 2012, the last time it offered insured 30-year amortizations on residential loans....

Bank of Canada Brings Back the Punch Bowl

Canadian borrowers will be toasting the BoC from coast to coast, having waited for this day since the first hike 27 months ago.

Odds are, today's 25 bps cut is just the appetizer. The Bank expects it to start a string of easing—one that markets anticipate will last about 200 bps.

Even though some naysayers called recent economic data "inconclusive," BoC chief Tiff Macklem couldn't ignore the red warning lights on his economic dashboard, nor (at least subconsciously) public cries for rate relie...

Ratehub's Founders to Reportedly Step Down

Fourteen years after redefining mortgage rate comparison, Toronto-based Ratehub is getting a fresh CEO.

Co-founders Alyssa Furtado and James Laird are reportedly passing the baton to Naga Parvatharaja. His last stint was as GM and Head of Lending at SoFi, a publicly traded U.S.-based "one-stop shop for digital financial services."

Parvatharaja inherits a business ripe with challenges but still brimming with potential....