You hear it all the time, "Rental properties don't cash flow anymore," like it's some kind of universal truth.

But not every new rental is a money pit waiting to devour your wallet.

For property investors who like to skate to where the puck

You hear it all the time, "Rental properties don't cash flow anymore," like it's some kind of universal truth.

But not every new rental is a money pit waiting to devour your wallet.

For property investors who like to skate to where the puck is headed, it's about seeing opportunities where others see a closed door.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

The Liberals served up their Fall Economic Statement (FES) yesterday and it's got multiple ramifications for mortgage borrowers and lenders. We've taken the liberty to grade our trusty rule makers on each of their mortgage-related moves.

The result? A smattering of A's - impressive.

The Liberals served up their Fall Economic Statement (FES) yesterday and it's got multiple ramifications for mortgage borrowers and lenders. We've taken the liberty to grade our trusty rule makers on each of their mortgage-related moves.

The result? A smattering of A's - impressive. But then, as unexpected as finding cheese on a pizza, there's one glaring F.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

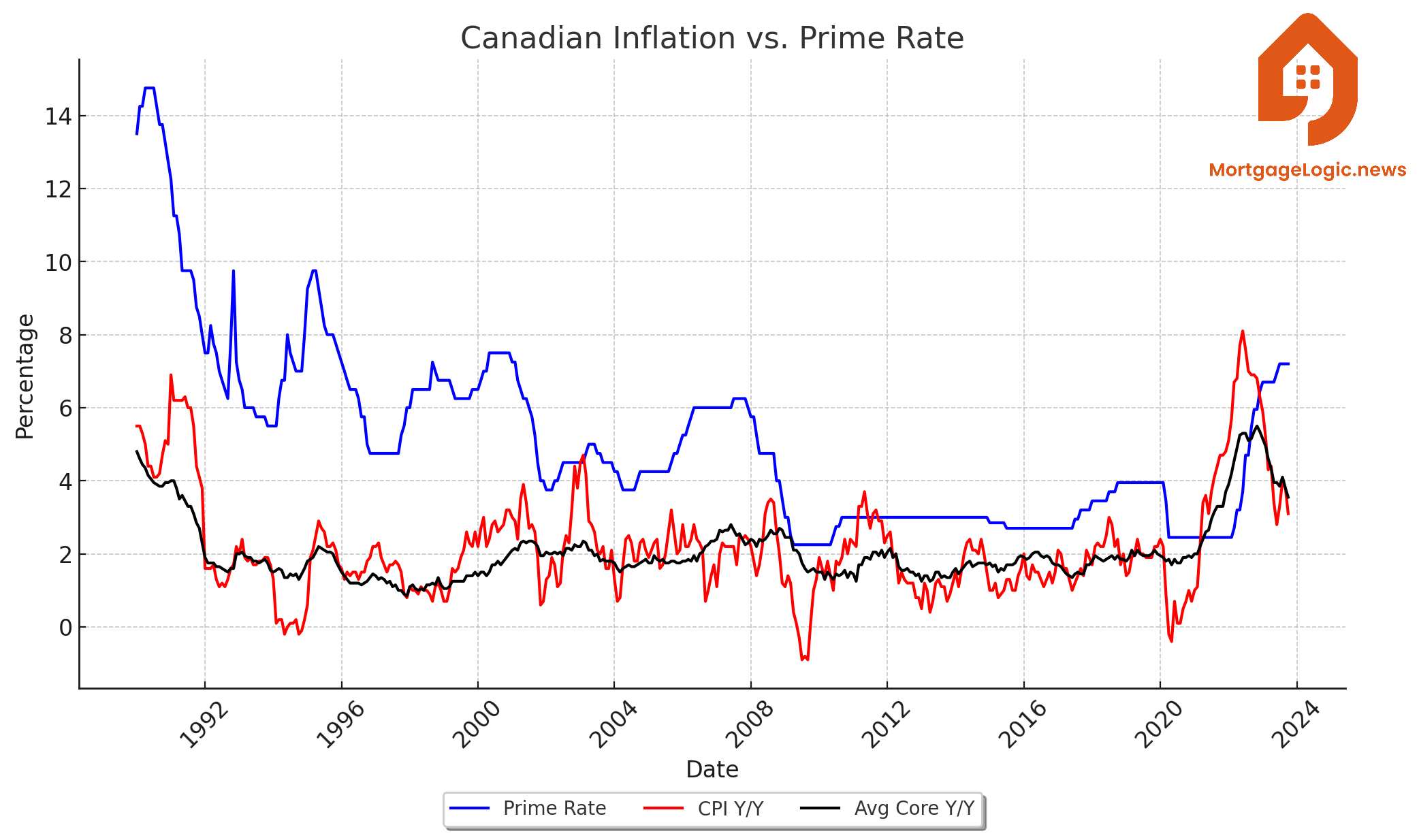

Out of the myriad of economic data, #CPI# is what matters most. And we made solid progress today. The question is, when will mortgage rates catch on?

What CPI did

Headline inflation, which usually hogs the spotlight, fell to 3.1% in October from 3.8% the prior month.

But

Out of the myriad of economic data, #CPI# is what matters most. And we made solid progress today. The question is, when will mortgage rates catch on?

What CPI did

Headline inflation, which usually hogs the spotlight, fell to 3.1% in October from 3.8% the prior month.

But the bigger star was the BoC's closely watched 3-month average core inflation measure. It dropped to 2.95%, the best reading since early 2021.

The cherry on top was the month-over-month change. BMO Economics notes that "in seasonally adjusted terms, prices fell 0.1%" in October. That's the first such decline since we all started hoarding toilet paper in 2020.

Mortgage interest cost and rent remain the main inflation drivers. The latter is more of a troublemaker than the former, given that rates should be on the downswing (infamous parting words).

"We expect headline inflation to fall to 2.0% by the third quarter of next year," said Stephen Brown from Capital Economics today. "With gasoline prices falling further in recent weeks, headline inflation is on track to drop below 3% this month."

It wasn't all a picnic in the park, however. Services inflation picked up, as did seasonally-adjusted inflation, excluding food and energy.

Canada's 5-year yield took the data in stride, falling just 3 bps on the day as of this writing. But it still managed to hit a low unseen since July.

Mortgage implications

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Our leaders have been swiping the national credit card like it's Black Friday, and mortgagors are paying the price for their extravagant spending.

Someone finally quantified that price last week when a Scotiabank report concluded:

"We estimate that government consumption and pandemic transfers to households account for

Our leaders have been swiping the national credit card like it's Black Friday, and mortgagors are paying the price for their extravagant spending.

Someone finally quantified that price last week when a Scotiabank report concluded:

"We estimate that government consumption and pandemic transfers to households account for about 200 basis points of the 475 basis points increase in the Bank of Canada’s policy rate."

Let's say Scotia's estimate is even half right. That's a whopping $17,000 extra that families are shelling out on a 5-year term (based on average mortgage amounts, according to TransUnion).

As much as some of that spending was justified to save families and jobs, much of it was our federal and provincial leaders acting like teenagers with a new VISA. The spending taps remain wide open, with federal program spending estimated at ~16% of GDP, well above the ~13% long-term average. How much the Liberals rein in spending will partly influence how far rates fall in the next rate-cut cycle.

But what many don't realize is, the riskiest spending is out of our control.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Bob Rennie is unquestionably one of the most successful real estate marketers in Canadian history. In his early days as a realtor, he was famous for selling a property a day. His development promotion expertise later earned him the nickname the condo king.

MLN soaked up Bob's insights

Bob Rennie is unquestionably one of the most successful real estate marketers in Canadian history. In his early days as a realtor, he was famous for selling a property a day. His development promotion expertise later earned him the nickname the condo king.

MLN soaked up Bob's insights on various real estate issues weighing on this country. Among other things, he shared:

Why home price declines are skewed

The biggest reason for housing unaffordability

The financing requirement that helped build Rennie's business

Rennie's "secret" to real estate marketing

How the foreign buyers' tax impacted the market

How the foreign buyers' tax elevated racism

Why Canadians need two properties to get ahead

How soaring rates in 1981 crushed him for years

His government-sponsored financing strategy.

Without further ado, here's our chat...

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

When Smith Financial bought out Home Capital, it necessitated that Home lose its precious NHA mortgage-backed securities (MBS) and Canada Mortgage Bond (CMB) allocations—i.e., the ability to fund its mortgages through MBS and CMBs.

That was a crushing blow to Home's prime mortgage competitiveness. After all,

When Smith Financial bought out Home Capital, it necessitated that Home lose its precious NHA mortgage-backed securities (MBS) and Canada Mortgage Bond (CMB) allocations—i.e., the ability to fund its mortgages through MBS and CMBs.

That was a crushing blow to Home's prime mortgage competitiveness. After all, the spread on CMB/MBS funding is just 25-50 bps more than the Government's risk-free borrowing rate. Lenders must add miscellaneous costs (guarantee fees, insurance premiums, etc.), but CMBs/MBS are still often the cheapest way to fund a mortgage.

Knowing this crucial lifeline would end, Home Capital chose to cut off its low-margin prime mortgage business like a gangrene-infected leg.

The loss of Home Trust as a prime mortgage competitor, in turn, led some to ask why this had to happen.

We turned to CMHC, the Yoda of securitization, for an explanation. It said...

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Credit unions are an afterthought for many Canadians. Yet, CUs are critical to the mortgage ecosystem because they compete in ways that banks don't.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

In the once stable world of mortgage market share, the Big 6 banks have slipped on a banana peel. Their market share of new mortgage originations sank 590 bps to 53.8% in Q1 2023, according to new CMHC data. That starkly contrasts with their previous 62.0%, from just

In the once stable world of mortgage market share, the Big 6 banks have slipped on a banana peel. Their market share of new mortgage originations sank 590 bps to 53.8% in Q1 2023, according to new CMHC data. That starkly contrasts with their previous 62.0%, from just two years back.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.