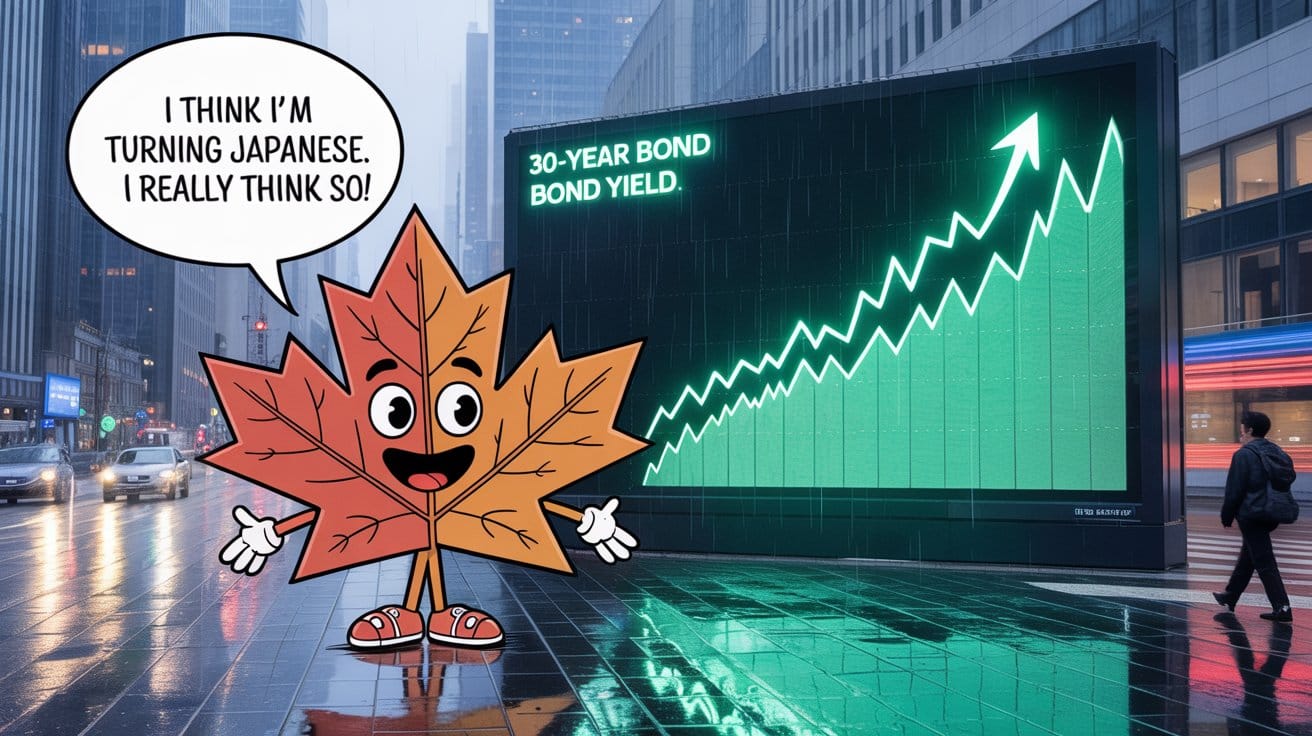

Last month, Japan's long-bond yields soared to unprecedented heights before temporarily retracing. Probably over 90% of Canadian mortgagors didn't even think twice about it, or once, for that matter.

Yet, Japan's debt challenges—while more extreme than most—mirror a global shift in the US$80 trillion government bond market. It may be setting up a future domino reaction that could be heading straight for everyone's wallets, Canadians included.

Back to top