⏩The short of it: Overpopulating and underbuilding is a recipe for absurd housing costs. Here's a look at six resulting implications, plus six opportunities for mortgage pros. For originators ready to dodge the stats and dive straight into dollar signs, the business strategy bits are near the middle.

The short of it: Overpopulating and underbuilding is a recipe for absurd housing costs. Here's a look at six resulting implications, plus six opportunities for mortgage pros. For originators ready to dodge the stats and dive straight into dollar signs, the business strategy bits are near the middle.

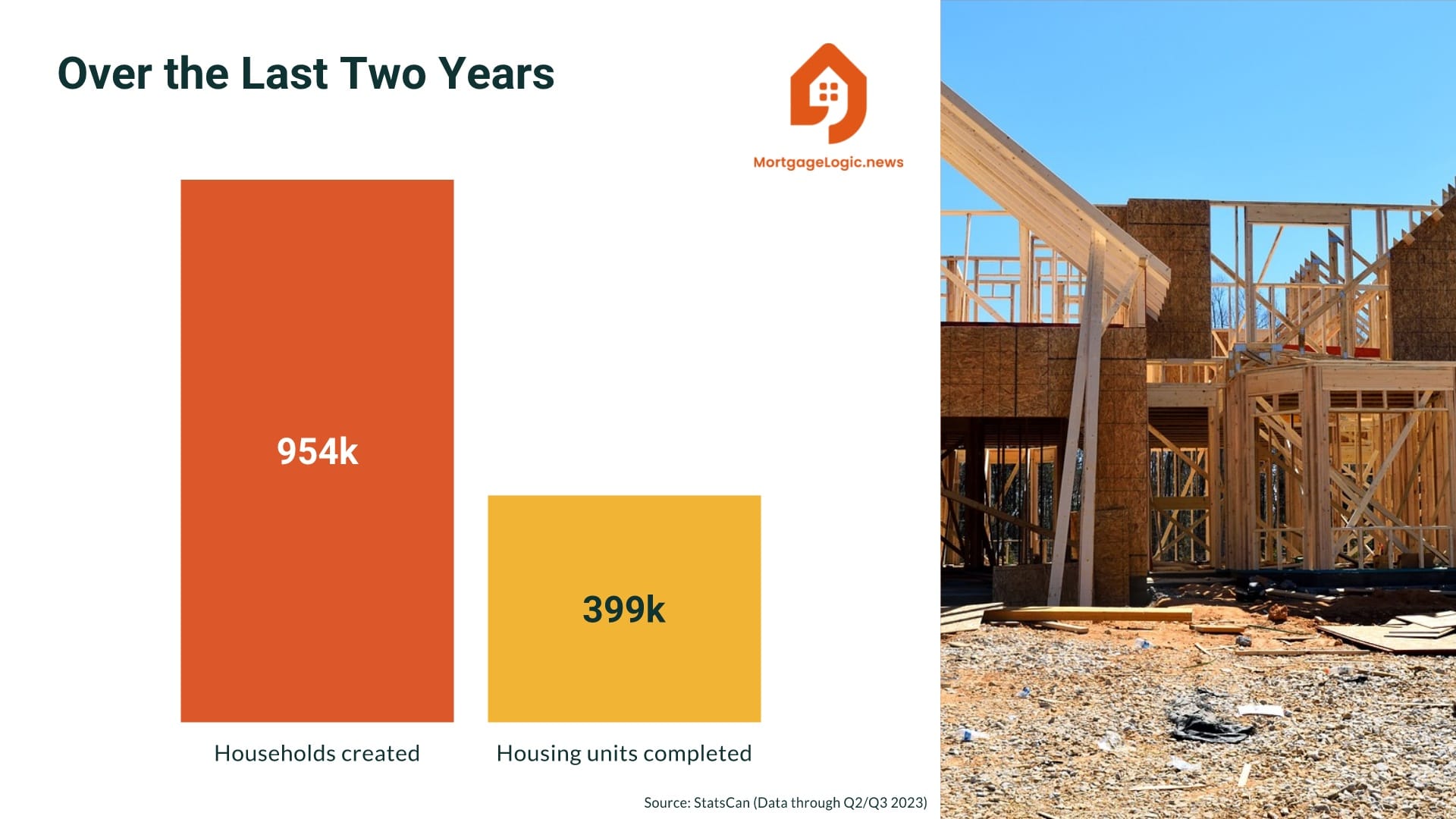

Canada is having a population party, and the invitations should read: BYOH — Bring Your Own House.

The latest numbers from StatsCan paint how badly our leaders are losing the fight to house our citizens affordably. To properly appreciate this train wreck, allow the following stats to sink in.

In the last 24 months of available data:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Rate cut optimism took a temporary detour today as inflation decided to stick it to economists. Instead of falling to 2.9% as Bay Street's number crunchers expected, it parked itself stubbornly at 3.1%.

The average core inflation reading was 3.45%, also refusing to budge from

Rate cut optimism took a temporary detour today as inflation decided to stick it to economists. Instead of falling to 2.9% as Bay Street's number crunchers expected, it parked itself stubbornly at 3.1%.

The average core inflation reading was 3.45%, also refusing to budge from last month's (revised) number.

But not all hope is lost. Here's why the mortgage rate glass is still half full:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

On Friday, it was "too early" for Bank of Canada head Tiff Macklem to consider rate cuts.

Four days later, he's ready to consider considering them. Macklem told BNN he now thinks BoC cuts will happen "sometime in 2024."

As Macklem does his monetary

On Friday, it was "too early" for Bank of Canada head Tiff Macklem to consider rate cuts.

Four days later, he's ready to consider considering them. Macklem told BNN he now thinks BoC cuts will happen "sometime in 2024."

As Macklem does his monetary moonwalk, the bond market is convinced he's not being forthright (which wouldn't be unusual for a central banker trying to suppress >3% inflation and inflation expectations).

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

If you're in the mortgage game—and serious about it—strategy planning for the coming year is an annual ritual. When crafting that plan, it never hurts to compare your outlook with that of big players in the mortgage origination space. And in Canada, they don't

If you're in the mortgage game—and serious about it—strategy planning for the coming year is an annual ritual. When crafting that plan, it never hurts to compare your outlook with that of big players in the mortgage origination space. And in Canada, they don't get much bigger than DLC Mortgage Group (DLCG).

We caught up with Gary Mauris, CEO of DLCG, who's been steering DLC's ship around the interest rate tsunami and housing storm. He gave us the lowdown on his team's 2024 mortgage expectations and a behind-the-scenes look at the company's internal optimizations.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Fed chair Powell is like the James Bond of central banking – licensed to thrill.

And did he ever. The Fed banker with the golden gun started the rate festivities early this week, leaving mortgage originators feeling like they just hit the jackpot.

The 2-year #GoC# yield—which often front-runs BoC

Fed chair Powell is like the James Bond of central banking – licensed to thrill.

And did he ever. The Fed banker with the golden gun started the rate festivities early this week, leaving mortgage originators feeling like they just hit the jackpot.

The 2-year #GoC# yield—which often front-runs BoC policy changes—dove with U.S. rates. It's now below its 18-month moving average (MA) for the first time since 2021 (chart below).

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

📰Canadian 5-year yields hit half-year lows following Fed announcement.

It was a bombshell down in Washington D.C. today. The U.S. Federal Reserve has just signalled that liquidity will return to the mortgage market in 2024.

In a policy swivel that few saw coming, Fed chief Jerome Powell confirmed

Canadian 5-year yields hit half-year lows following Fed announcement.

It was a bombshell down in Washington D.C. today. The U.S. Federal Reserve has just signalled that liquidity will return to the mortgage market in 2024.

In a policy swivel that few saw coming, Fed chief Jerome Powell confirmed the Fed has already begun discussing when to "dial back" rate hikes—not that they will in the near future. To markets, that's the Fed effectively endorsing the peak rate thesis.

Canadian yields, moving in sympathy with Treasuries, plunged faster than Charlie Sheen's career after Two and a Half Men. The 5-year #GoC# is down 21 bps as we speak. We're hitting lows we haven't seen in half a year. On a point basis, today is the most significant drop since the March madness with U.S. banks.

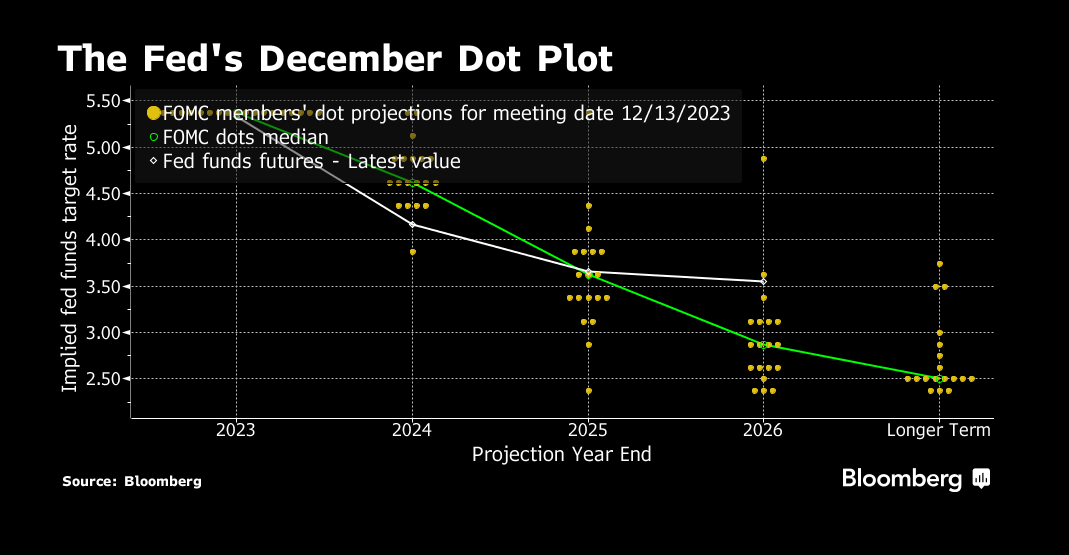

The New Crystal Ball: Rates Edition

Source: Bloomberg

Fed headliner Powell took to the stage in his presser and talked about "real progress in core inflation." As a result, #FOMC# members now see 75 bps in cuts in 2024 and more easing in 2025.

In Canada, market expectations are approaching five (5) rate cuts in 2024 (no joke), with the first in April. Here's the latest expected BoC rate path, as implied by Canada's #OIS# market.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡OSFI left its minimum qualifying rate (MQR) at 5.25% on Wednesday. Details below...

Trying to bring inflation back to 2% is starting to feel like trying to lose weight over the holidays—tough sledding.

Wednesday's U.S. CPI report was a reminder of that. Headline inflation ticked

OSFI left its minimum qualifying rate (MQR) at 5.25% on Wednesday. Details below...

Trying to bring inflation back to 2% is starting to feel like trying to lose weight over the holidays—tough sledding.

Wednesday's U.S. CPI report was a reminder of that. Headline inflation ticked down a notch to 3.1% from the previous 3.2%, moving with the urgency of a turtle herd. But core inflation seems to have attachment issues. It's been stuck in the 4.0 to 4.1% range for three months.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

For many in the business, 2023 was to the mortgage sector what pigeons are to statues.

Fortunately, the slate wipes clean in less than a month. With rate relief on the horizon and December volumes as slow as Toronto traffic, there's no better time to strategize on expanding

For many in the business, 2023 was to the mortgage sector what pigeons are to statues.

Fortunately, the slate wipes clean in less than a month. With rate relief on the horizon and December volumes as slow as Toronto traffic, there's no better time to strategize on expanding your presence, increasing efficiencies and fortifying your brand.

Here's a hit list of 25 tactics that might do just that. Not every tip will fit, but you'll probably find a couple to build your mortgage muscle in 2024.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.