Borrowers are often told that different things drive fixed and variable mortgage rates. The Bank of Canada guides variable rates, mortgagors are told, while the bond market steers fixed rates.

That's largely true, but fixed and variable rates are actually more siblings than distant cousins.

Borrowers are often told that different things drive fixed and variable mortgage rates. The Bank of Canada guides variable rates, mortgagors are told, while the bond market steers fixed rates.

That's largely true, but fixed and variable rates are actually more siblings than distant cousins.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡Mortgage Bytes follow below...

Canada's FINTRAC rules have hit the mortgage broker industry like a piano falling from the sky. Almost three weeks after FINTRAC started in the mortgage industry, we're getting emails from brokers at top brokerages still confused about their obligations. This includes brokerages

Canada's FINTRAC rules have hit the mortgage broker industry like a piano falling from the sky. Almost three weeks after FINTRAC started in the mortgage industry, we're getting emails from brokers at top brokerages still confused about their obligations. This includes brokerages that tout their compliance records, which shall remain nameless. It's a good thing no one's getting audited for a while because industry failure rates might be north of 1 in 4.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Some banks are hawking popular 3-year terms for 4.14% to 4.29%, or even less for fat loan amounts.

In some instances, for strong borrowers with $600,000+ loan amounts, leading status brokers are getting 3.99% on discretion. We've seen multiple commitments at that rate in

Some banks are hawking popular 3-year terms for 4.14% to 4.29%, or even less for fat loan amounts.

In some instances, for strong borrowers with $600,000+ loan amounts, leading status brokers are getting 3.99% on discretion. We've seen multiple commitments at that rate in the last 10 days. Select banks have been that generous even for uninsured mortgages.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Trudeau has finally done the right thing and moderated immigration levels. That means more first-time homebuyers might actually get to own something bigger than a U-Haul storage unit.

It also means real estate doomsdayers are doing victory laps as we speak. For those who thought Canadian real estate was a

Trudeau has finally done the right thing and moderated immigration levels. That means more first-time homebuyers might actually get to own something bigger than a U-Haul storage unit.

It also means real estate doomsdayers are doing victory laps as we speak. For those who thought Canadian real estate was a Ponzi scheme built on immigration, this is their "I told you so" moment.

After taking due time to digest the government's immigration bombshell, however, nothing seems particularly apocalyptic about the new immigration targets. That is, unless you own a big city shoebox condo (or sell them). In that case, keep your Xanax prescription current.

Overall, we're still cautiously optimistic for Canada's mortgage market and real estate in 2025, but admittedly more downbeat on 2026.

If you're a mortgage stakeholder worried about origination volumes or a property investor nervous about real estate ROI, read on. The Q&A that follows breaks down the possibilities and is light on economic double-speak.

Question: How much will population change?

Answer: The government says Canada will lose population (0.2%) over the next two years. If we recall correctly, the last time that happened was the fourth of never.

This is a complete 180 from last year, when the feds stuffed 3.2% more people inside our borders. That's 1.27 million to be exact, enough to populate a city the size of Calgary.

As for negative growth, some economists (e.g., BMO and Scotiabank) don't buy it. They're betting Ottawa will execute this plan with all the precision of a toddler with chopsticks, predicting flat to 0.5%+ growth instead.

Either way, the chart below will finally start dropping—and fast.

Question: How big a deal is the permanent resident change?

Answer: It's like finding a bug in your supposedly "triple-washed" bag of lettuce - not great, but we'll live. 395,000 immigrants in one year still towers over anything Canada saw prior to the pandemic, save for 1913 when 400,000 immigrants showed up looking like extras from Peaky Blinders.

Toronto, 1913

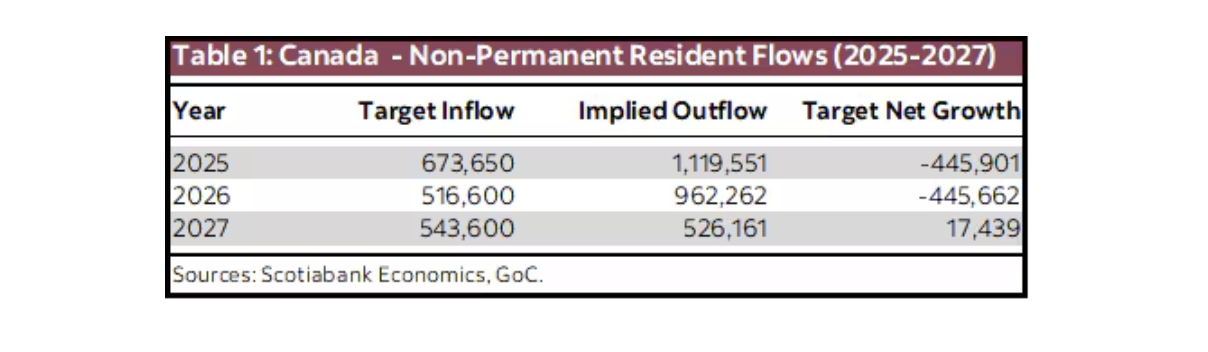

Question: How big a deal is the change in non-permanent residents?

Answer: Oh, you're definitely going to notice. A 900,000 decline in temporary residents is unprecedented and will have economic ripple effects.

Table courtesy of Scotia Economics

However, before you panic-dial your realtor to list, consider this:

Ottawa is still rolling out the welcome mat for newcomers from abroad (only 40% of future permanent residents are already here).

Permanent resident households contribute more to the economy per capita than temps. For one thing, most permanent residents buy homes. Only 15.3% of non-permanent residents (NPRs) are homeowners. Of course, investors buy properties to rent to NPRs, but that's far from the majority of demand in over 9 out of 10 markets.

Going forward, a slightly greater share of newcomers will be from the higher earning "economic class."

There's a chance Team Trudeau exceeds its targets to keep the economy afloat in an election year.

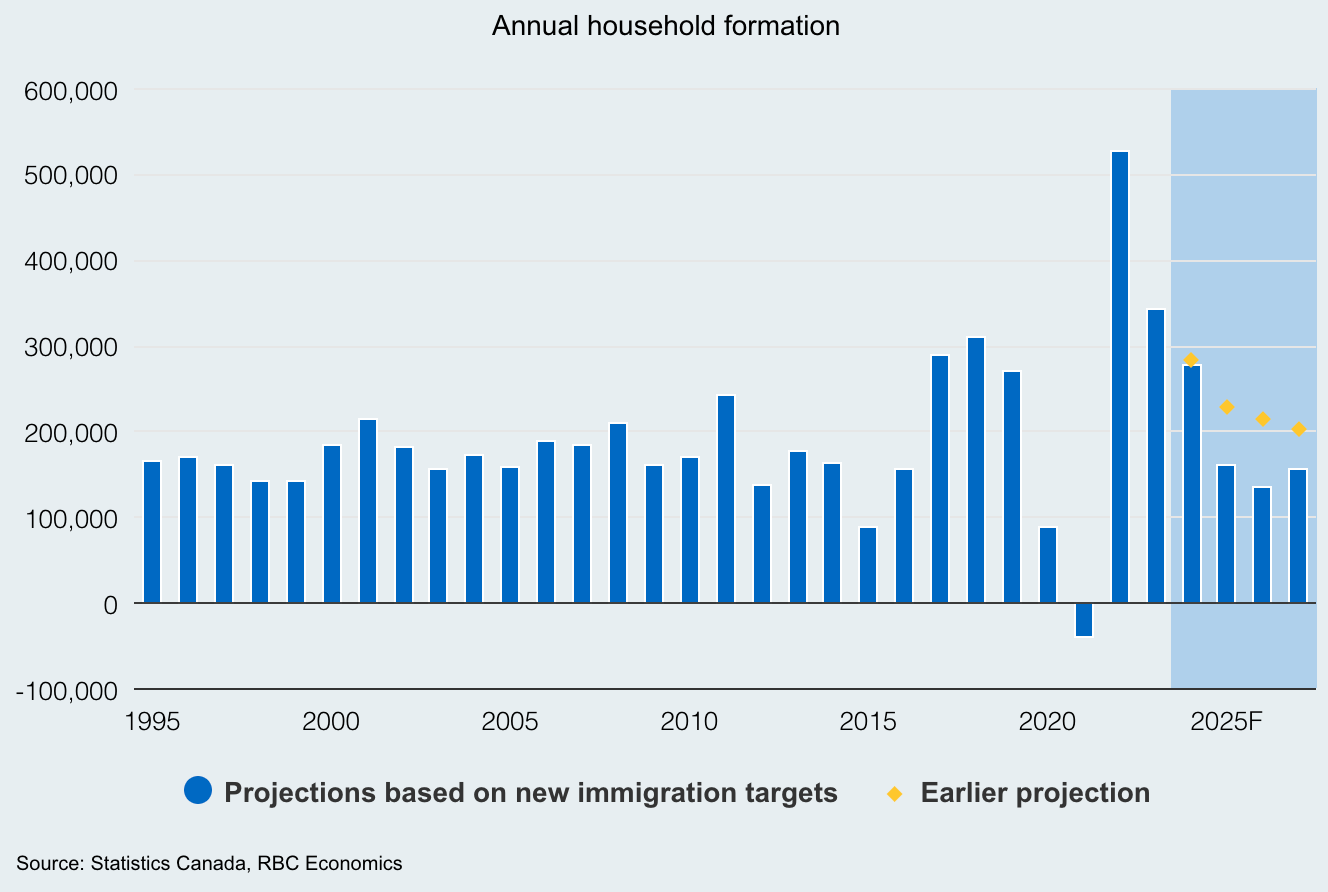

Question: How much will household formation decline?

Answer: It shouldn't. If RBC's forecast is half as accurate as its overdraft fees, annual household formation—a driving force for residential investment, home appreciation and mortgage growth—will stay in the black.

Chart courtesy of RBC Economics

Question: How will Canadian growth be impacted?

Answer: Conventional thinking is summed up by this Capital Economics comment:

"The net result of the immigration policy change still seems to be that the Bank [of Canada] will need to take interest rates lower in order to secure a rebound in GDP growth that closes the output gap and prevents consumer price inflation from falling too far."

RBC thinks multiple rate cuts are a shoe in, given the Liberal's plan could trim growth by "nearly a percentage point "over the next three years."

As for the BoC, before the immigration announcement, it projected 2.1% GDP in 2025. Upon learning of the Liberal's plan (did Trudeau really not tell Governor Macklem before Wednesday's rate announcement?), Tiff conceded:

"If population growth comes down faster than we have assumed, headline GDP growth will be lower."

And while we're on the topic of groundbreaking revelations, the Captain would like to remind you that, "less is less and lower is lower."

Meanwhile, Scotia Economics—wielding spreadsheets like they're solving cold fusion—estimates we need 0.85% population growth just to stay “productivity-neutral.” By 2026, that seems unlikely unless a new government reshuffles the immigration deck.

The economic takeaway, as Captain O. would note, is that fewer immigrants spending money hurts growth.

Fortunately, rate cuts are an antivenom for that. As a rough rule of thumb, every 100 basis points the BoC drops is good for at least a 50 to 100 bps GDP boost within 12-24 months.

Question: Okay, but will depopulation fuel or suppress inflation?

Answer: Immigration's impact on inflation is complicated.

Responding to reporters, Macklem said:

“The inflation forecast itself is not that affected by population growth...There could be some [downward] effect, but population growth affects both demand and supply.”

Indeed, inflation—excluding shelter—is already tracking under 1% y/y, says BMO. Rent deflation alone (from less rental demand and more supply) could largely diminish the threat of accelerating CPI.

But one less source of upward pressure doesn't mean inflation must drop significantly. Consider that:

A combination of the following could be far more consequential: fiscal spending, potential dollar depreciation, drastic energy price moves, more global supply shocks, unanticipated wage growth, and trade frictions (hello, Trump).

There's always the chance of unexpected organic growth from eased financial conditions, mortgage loosening, rising incomes, etc.

As our population slows, monetary policy will get more stimulative. The two could offset. (BoC easing takes 12-24 months to change the course of inflation, and we're already well down the easing path.)

As population slows, labour force growth slows or even shrinks. That means less unemployment, #OTBE#.

A falling population also means employers will lose workers faster. Less labour supply potentially means higher wages—a key inflation driver. That's especially true for NPR-heavy sectors like tourism, hospitality, hotels, bars, restaurants, and agriculture, says Scotiabank.

"If the slower pace of population growth helps improve shelter affordability, households might have more cash available to spend in other areas of the economy," Desjardins wrote this week. That, too, supports overall price levels.

All of the above could counteract the disinflationary effect of an immigration clampdown. That's why predicting inflation one to two years out is like peeing in the dark (forgive the expression). There's no way to know how it'll turn out.

While newcomers do support demand, they're just one cylinder in Canada's economic engine. Macklem, with all the cool of a bond trader holding AAA securities, downplayed the disinflation risks on Friday, saying: "There could be some timing effects, but they are pretty second order."

Question: What about mortgage rates?

Answer: The most prescient rate predictor in existence is the bond market. It's got more data processing power than 1,000 Bank of Canadas, and it prices in all knowable information.

What's the bond market's conclusion after this immigration hullabaloo?

It's pricing in fewer BoC cuts, not more. The market-implied trough rate of this cycle was 2.50% last week. It closed yesterday at 2.75%.

That's not to say it won't change or bond traders can't be wrong, but the market-implied outlook beats almost all individual forecasters over the long haul.

There's also a bit of upside rate risk from rising deficits, which now seem more likely with less population growth to boost GDP and government revenues.

So, yes, variable rates will drop further, and probably fixed rates too. And yes, floaters still perform best on paper based on the forward rate outlook. But there's nothing to guarantee that: (A) life-changing, low borrowing costs are around the corner, or (B) rates will stay low for long, if/when they hit neutral.

Question: Is there any upside for mortgage volumes?

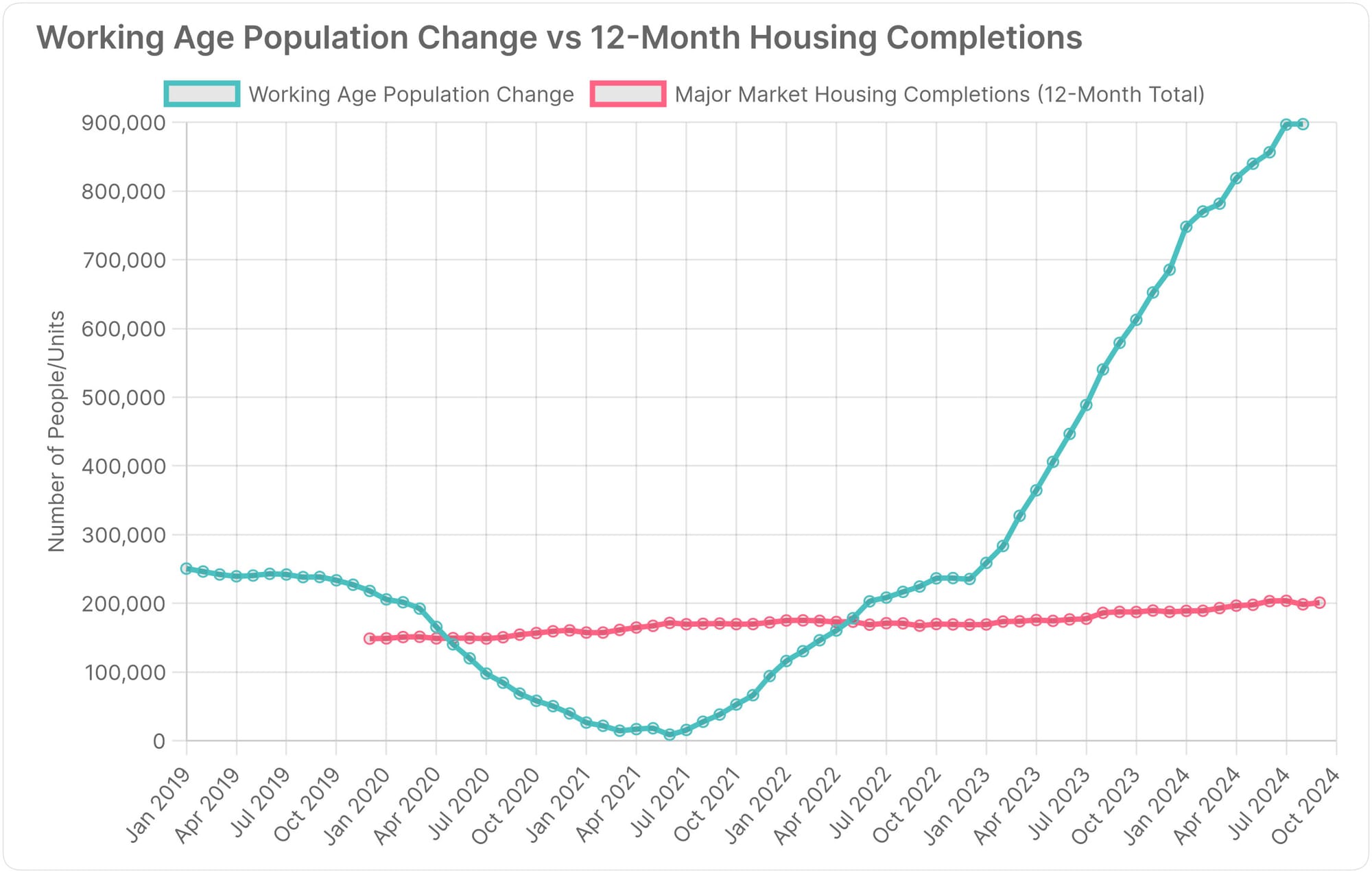

Answer: Yes. Like the 90s band Oasis, home affordability is staging a comeback. And if employment and incomes hold up and people can afford homes, they'll get mortgages. While no one can reliably predict overall home sales in 2025, transaction volumes should rise for that particular segment.

That said, immigration reductions are less meaningful than aggressive rate cuts. Another 100 bps off the overnight rate (the market's projection) will counteract much of Canada's slowing headcount.

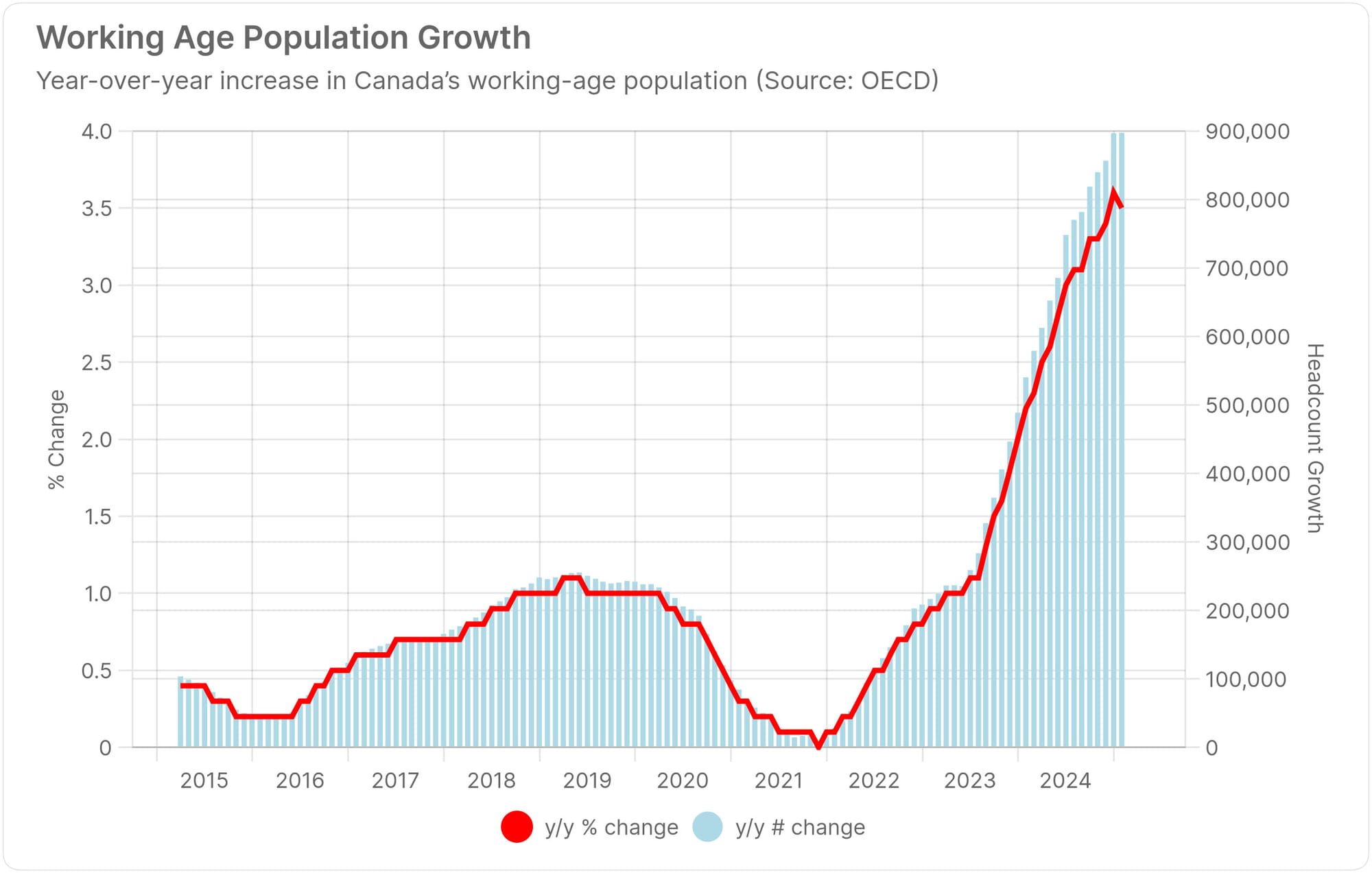

And like Oasis fans lining up for tickets, Canada's got a lineup of eager homebuyers—immigrants and non-immigrants—waiting for affordability to purchase. The below chart of working-age population growth illustrates just some of that buyer backlog.

"Among the G7 nations...Canada suffers the lowest average housing supply per capita at 424 units per 1,000 residents," writes Concordia University's Erkan Yönder in a recent study. As more supply becomes available relative to the population, sidelined buyers should jump on it (which translates to additional mortgage applications).

Question: Should I be worried as a landlord?

Answer: In some markets, yes. This news may flush out weak hands from big city condo markets. Another pickup in apartment listings should be expected.

Landlords in some immigration-heavy markets are now staring at:

A 900,000 nosedive in NPRs — it's like losing a large city of renters in the next two years

A 21% drop in new permanent residents (PRs typically rent first, ask questions later)

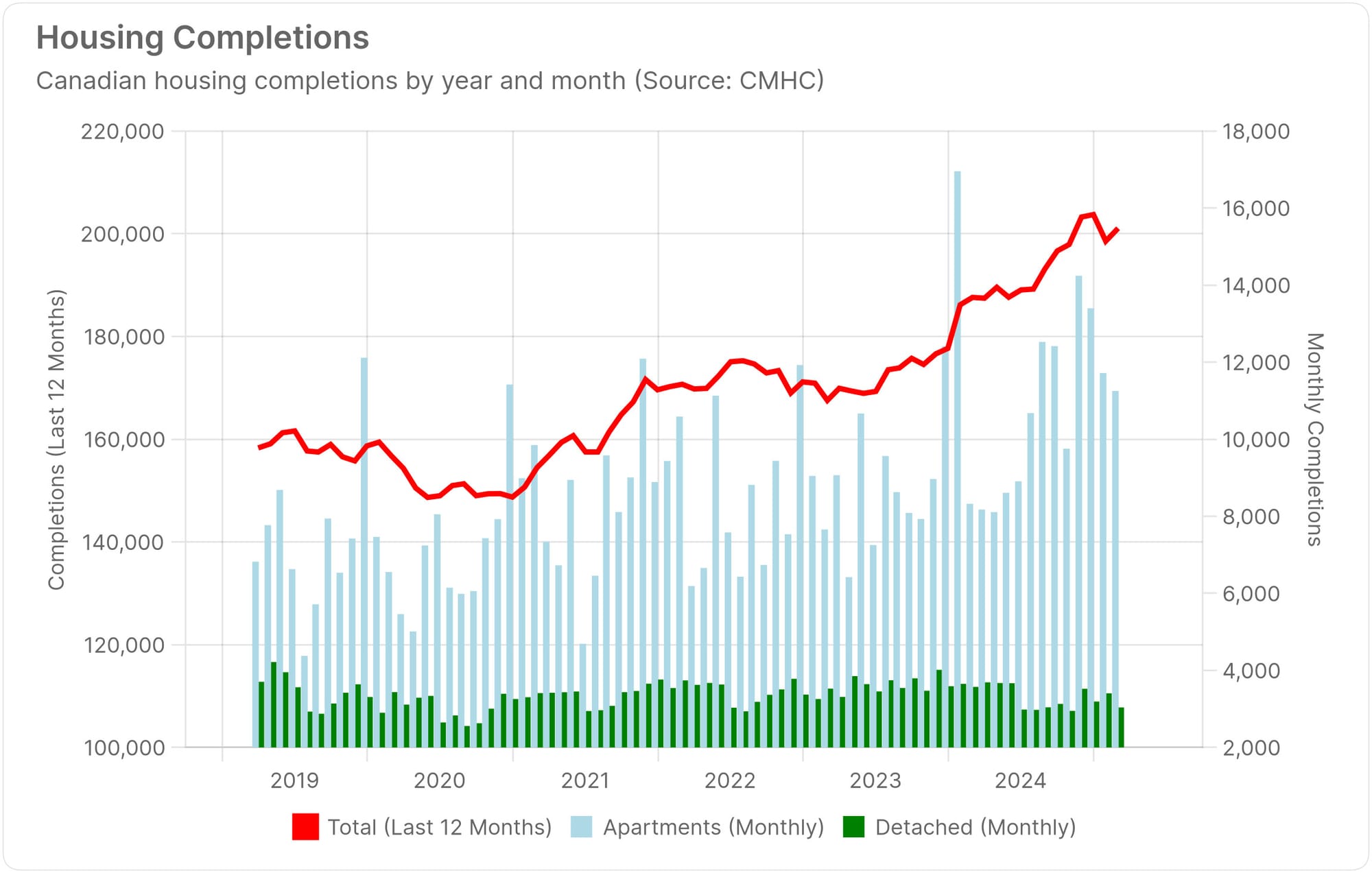

Record multi-unit completions

Big construction pipelines (e.g., 90k apartment units are currently being built in the GTA)

A 17%+ y/y jump in listings (CREA national data)

The chilling ruling that just affirmed CRA's right to charge up to 13% tax on the sale of homes used for short-term rentals—making Airbnbs as appealing as penny stocks

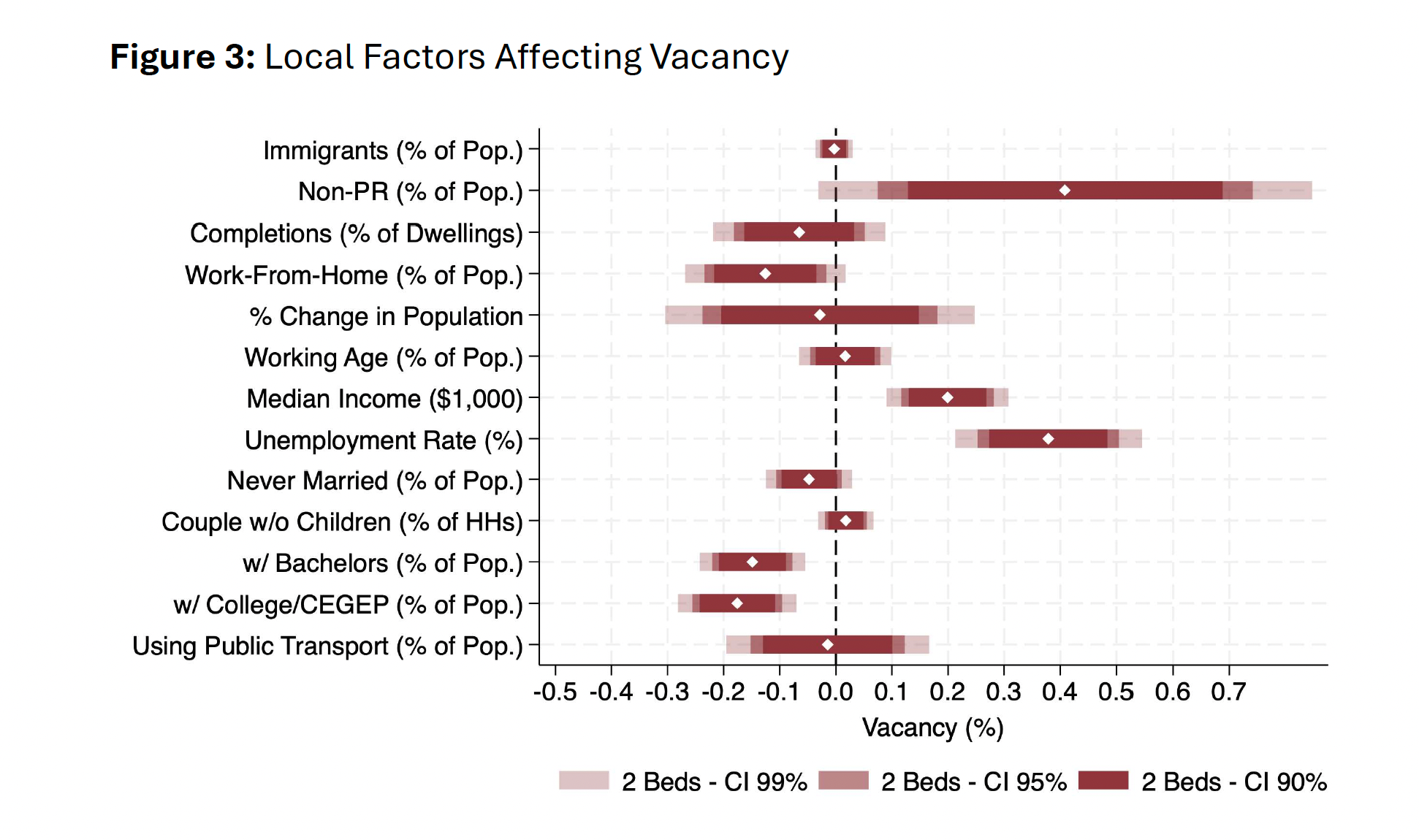

Rising rental vacancies—a problem even before the cutback in non-permanent residents (NPRs are the #1 vacancy driver, per this study below from Yönder).

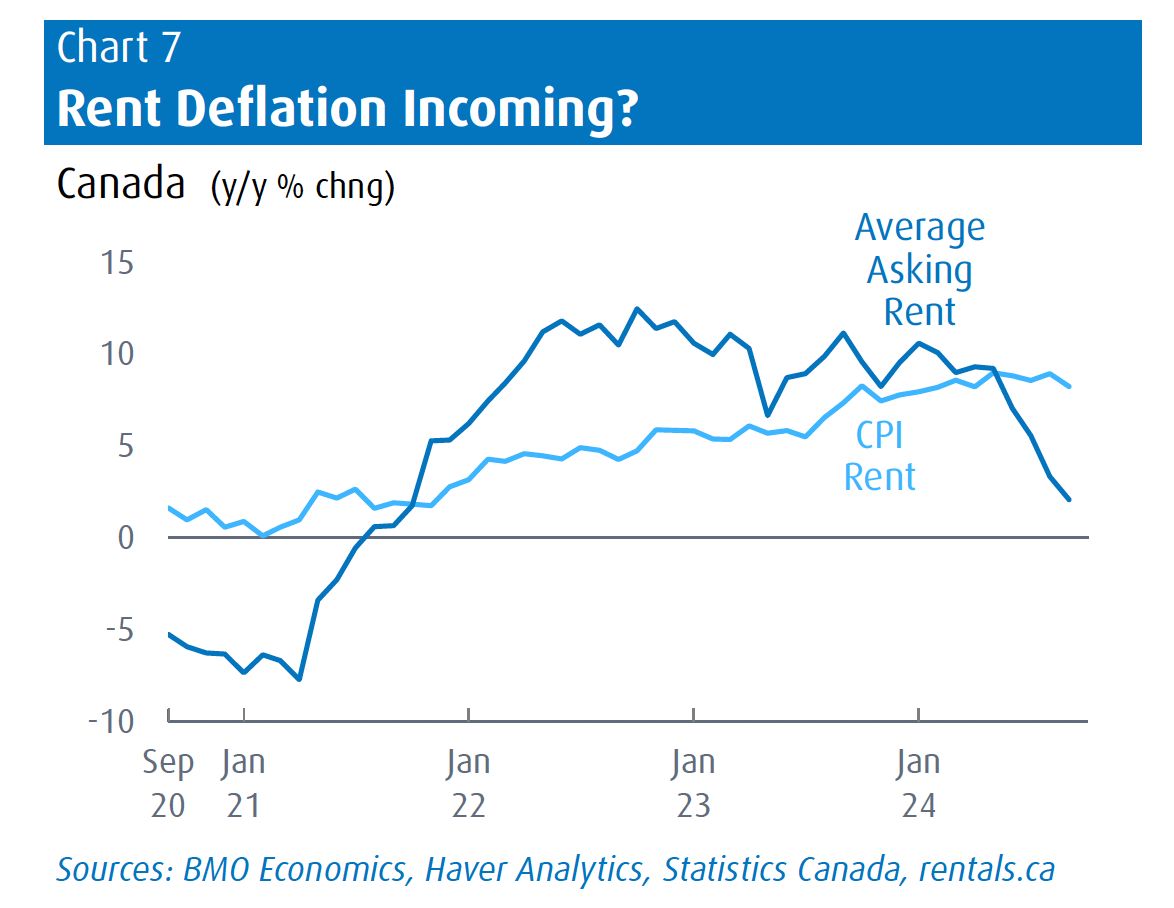

Housing analyst Ben Rabidoux, in his always readable Edge Analytics report, predicts "vacancies could potentially go "from record lows in 2023 to record highs by 2027."

Chart courtesy of BMO Economics

In short, many big-city investors will need to dial down their ROI expectations—at least until prices adjust.

But, remember the golden rule: location, location, location. Fast-growing markets that aren't as immigration reliant could still present value. This is particularly true for regions with robust interprovincial migration, such as parts of Alberta, B.C., and the East Coast.

Either way, Canada's rental market isn't dead - it's just got a case of market flu. Patient investors with cash may find some profitable deals in 2025/2026.

Question: What's the likely impact on home building?

Answer: By the government's estimates, the housing supply gap is "expected to decrease by approximately 670,000 units by the end of 2027."

We have to wonder if they, or anyone, really have a clue what the housing deficit is. But regardless, there's more to the story.

"Lower population growth will...significantly reduce the incentive for new home construction," predicts Capital Economics. It's a classic catch-22 that will work against Ottawa's home-building ambitions.

So will the fact that lower immigration shrinks the construction workforce. Expect that to further constrain home supply and ultimately support prices.

Over in the single-family arena, it's a different ballgame. Even with big city condos selling like ice cubes in the Arctic, balance in the detached market will be harder to come by. There's just not enough product (see below) vis-à-vis the last three years of population gone wild.

Question: What's the likely impact on home prices?

Answer: We don't have to tell anyone what less housing demand (in isolation) means for the direction of home values. Immigrants have accounted for between 1 in 5 to 1 in 3 home purchases in recent years.

Here's the kicker, though - the large majority of immigrants buying in the next few years are already in Canada. That's because most newcomers spend years renting before buying their slice of the Canadian dream.

In short, there's still a backlog of future buyers. That's why the sentiment hit from this news might be the bigger risk to values in the weeks ahead than an actual demand deficit.

Ultimately, outcomes depend on the type of home (condo, single-family, townhome, etc.), location and supply response. Condos in Toronto, Vancouver and the Fraser Valley could be in trouble. Single-family homes, not so much—particularly if the average mortgage qualifying rate drops back to 5.25% and borrowers can leverage more.

Regardless, homebuyer sentiment plays a role in prices. In most big cities, we'll see investors retreating faster than economists from failed predictions. Finding a multi-unit rental with good ROI potential will require surgical precision in the next 18 months.

But look - rates are sliding, and immigration's set to bounce back in 2027. Any resulting downturn shouldn't be long-lasting—unless there are other surprises, like inflation going rogue or a deficit-driven yield surge. Primary residence real estate remains a solid long-term tax-free investment.

In sum

Despite many knee-jerk assumptions, Canada's population growth won't imminently vanish. But that won't stop chicken littles from running out of their coops, clucking about how real estate's sky is falling.

"The government’s [population decline projections] appear to be Q4/Q4 growth rates," says Capital Economics. "Thanks to strong immigration over the course of this year and potentially in the first quarter of 2025 too, the government’s targets still seem consistent with a positive annual average population growth rate of just below 1% in 2025."

That's a level-headed outlook that hopefully pans out.

In any event, real estate returns may not be the layup Canadians are used to for the next few years. But that too shall pass.

For one thing, population growth isn't optional for an aging economy with a low birth rate, so it will be back.

For another, the old or new government is bound to calibrate the PR/NPR admission numbers next year.

And lastly, Ottawa protects home values like banks guard their trading algorithms. The last thing policymakers want is tanking home values creating financial system drama.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.