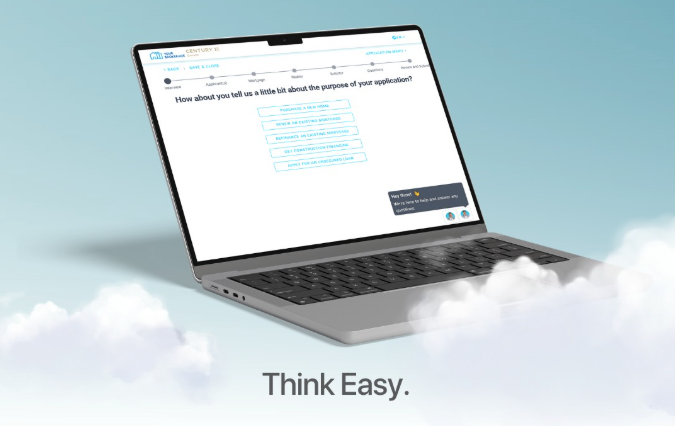

Building a client mortgage portal has traditionally required a lot of time-consuming and expensive coding. Not anymore. Tools like Scarlett 3.0, a client portal builder for mortgage brokers, have made the process far simpler, faster and less expensive.

Scarlett 3.0 debuted last month for Scarlett Mortgage (POS) users. Here's a quick rundown of eight useful new features that can either make/save brokers more money or keep their customers happier:

Back to top