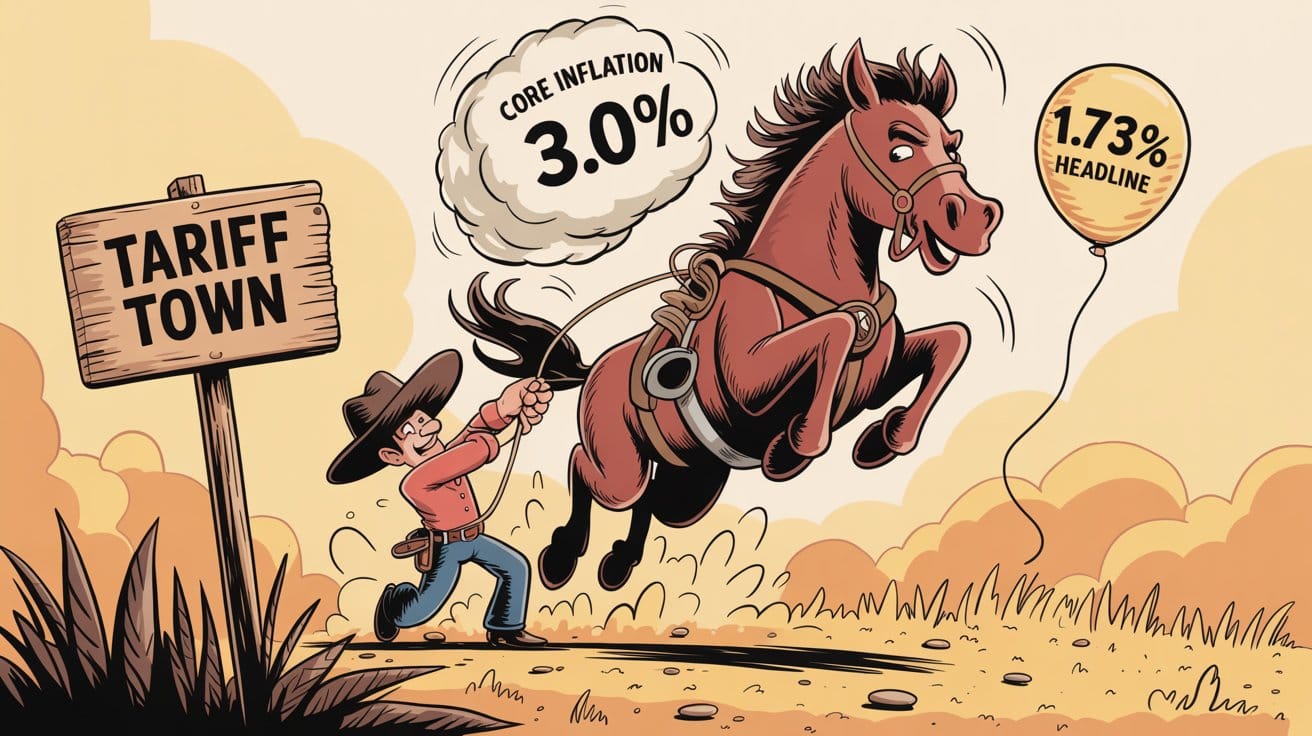

Yields had a mini bout of bipolar disorder on Tuesday. First, they shot up after the above-target core inflation print. Then, they pulled a complete reversal and tailed American yields lower.

Here's a closer look at what swayed Canada's 5-year yield, and in which direction:

Yields had a mini bout of bipolar disorder on Tuesday. First, they shot up after the above-target core inflation print. Then, they pulled a complete reversal and tailed American yields lower.

Here's a closer look at what swayed Canada's 5-year yield, and in which direction:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

As some of you have already heard, Equitable Bank CEO and industry trailblazer Andrew Moor passed away without warning this weekend.

It was a shock to everyone who's been in this business for more than a few years. The reason: he was one of the finest members of

As some of you have already heard, Equitable Bank CEO and industry trailblazer Andrew Moor passed away without warning this weekend.

It was a shock to everyone who's been in this business for more than a few years. The reason: he was one of the finest members of Canada's mortgage community—widely respected, good-natured, forthright, and passionate about helping Canadians save more money.

If you didn't know Andrew well, here's a small glimpse into how he operated, how industry leaders remember him, and what's next for the company he helped build.

Decades of service to Canadian borrowers

Andrew had been the chief visionary at Equitable since joining the firm in 2007, back when it was just a small alternative Trust company.

He grew Equitable from $3 billion in assets to a "Challenger Bank" with $127 billion.

Andrew left behind a lasting legacy. Not only did he advance no-branch banking to the next level with innovative digital-first offerings, but he also fought for the infrastructure that multiple fintechs rely on to challenge the Big 6. Andrew was a critical voice for advancing Canada's open banking initiative, despite the painfully slow bureaucracy.

"The world of banking in Canada is a better place because of his efforts," said spokesperson Maggie Hall on Tuesday. "Whether Canadians knew of him or were EQ Bank or Equitable Bank customers or not, they benefited from his relentless belief that Canadians deserve more."

Industry remembrances from across the country quickly started pouring in after the news broke.

Gary Mauris, Co-Founder and CEO of DLC Group, shared the following this morning:

"The loss of Andrew Moor has left a deep void in our hearts and in the Canadian banking community. His passing is a true gut punch, a pain felt by all who had the privilege of knowing him. Andrew was a lovely man, full of warmth, with a hearty laugh that could light up a room and a loyalty that was unwavering. A true icon in the Canadian banking space, Andrew was more than a leader—he was a friend, a passionate advocate for brokers, and a visionary who shaped the industry with his integrity and dedication. Andrew’s legacy will live on in the countless lives he touched, the innovations he championed, and the kindness he extended to everyone around him. He will be sadly missed!"

Luc Bernard, Chairman and CEO of M3 Financial Group, shared this:

We were deeply saddened to hear of the passing of Andrew, and on behalf of the entire M3 Group team, I want to express our most sincere condolences to Andrew’s family, friends and colleagues. As a past President and CEO of Invis, I always considered Andrew as part of the M3 family — he has been a true visionary who helped shape not only the direction of Equitable Bank and EQ Bank but the evolution of our entire industry. His forward-thinking, sharp insight, and relentless pursuit of innovation left an indelible mark on all of us who had the privilege to work with him. He inspired us not only with what he accomplished, but with the way he led — with clarity, integrity, and heart. On a personal level, I am truly grateful for the time we shared on numerous initiatives as he was someone I considered a friend. His legacy will continue to live on in the work we do every day.

Yousry Bissada, Andrew's former counterpart as CEO of Home Trust, said this:

"Andrew truly loved the banking industry, but even more so, he cherished his family. His pride in them was always evident. It was a pleasure serving alongside him on various associations, where his deep understanding of proposed rules and regulations consistently elevated the conversation. He always brought thoughtful, constructive feedback to the table, ensuring that regulatory policies supported both competitiveness and practical execution in Canadian banking. Andrew’s dedication to improving the banking landscape for all Canadians was steadfast and inspiring. I am very sad for this loss."

Andrew Moor

Andrew also had a strong sense of duty to his investors. He knew how vital low funding costs were to a challenger lender's success. He created the most diversified funding model of any non-Big 6 bank, including digital EQ Bank retail deposits, wholesale funding, credit union alliances, brokered deposits, NHA securitization and covered bonds. That's just part of the reason Equitable's stock soared 2,100% since the financial crisis under his leadership.

A top bank analyst that MLN spoke with this morning remembered him this way, "He was a quality CEO ... did a great job building the mortgage business post-#GFC# and EQ Bank over the past 10 years. He always had time for me, whether it was a phone call or meeting, or supporting our client events."

Before his run at Equitable, Andrew was President of mortgage brokerage firm Invis (which HSBC acquired in 2005 under his leadership) and Chair of the Canadian Association of Accredited Mortgage Professionals (CAAMP).

No cause of death was released, but sources report it to have been a heart attack while exercising this weekend. Andrew reportedly battled with atrial fibrillation and was nearing retirement. He was 65.

💡

For more on his business philosophy, here's a video interview that MLN did with Andrew back in 2023.

Next steps for Equitable Bank

"We view this unexpected development negatively as Mr. Moor had a central role in the growth of the bank...," said bank analyst Darko Mihelic in a report this morning.

On an interim basis, Marlene Lenarduzzi, Equitable Bank's current chief risk officer, has been named CEO, effective immediately. The company notes that, "She has more than 25 years of experience in risk management and banking strategy development, as well as experience in regulatory affairs, risk quantification, operations and execution."

"Andrew and the Board of Directors had been working closely together on succession planning for the past few years," explained Hall. "This process was very advanced at the time of his passing, and the Board expects to be able to announce his permanent successor in the very near term."

Whomever that person is, they'll have an incredible legacy to uphold.

From all of us at MLN, our deepest sympathies go out to Andrew's family and the co-workers lucky enough to have worked with him.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

After the U.S. decided diplomacy meant blowing up Iranian nuclear facilities this weekend, here's what moved Canada’s 5-year yield, and in which direction:

After the U.S. decided diplomacy meant blowing up Iranian nuclear facilities this weekend, here's what moved Canada’s 5-year yield, and in which direction:

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Rates ended the week on a down note as retail sales flopped like a fish on a dock. Here's a quick unpacking of what drove Canada's 5-year yield on Friday.

Rates ended the week on a down note as retail sales flopped like a fish on a dock. Here's a quick unpacking of what drove Canada's 5-year yield on Friday.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Brokers prefer to get paid full commission on every deal, but it doesn't always work that way. Sometimes, even those who’d rather wrestle an alligator than offer a buydown end up shaving their pay or kissing a deal goodbye.

That brings us to a recent case where

Brokers prefer to get paid full commission on every deal, but it doesn't always work that way. Sometimes, even those who’d rather wrestle an alligator than offer a buydown end up shaving their pay or kissing a deal goodbye.

That brings us to a recent case where a broker lost a deal after being undercut by a TD rep. It was publicized in a private industry forum, with some swearing it proved TD’s got a vendetta against brokers.

Now, we're not trying to choose sides, but here's what that “banks have it in for brokers” line of thinking totally misses.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

💡See also: 5yr Yield Unchanged With U.S. Bonds Closed + Mortgage Tidbits

CIBC has quietly pulled the plug on the mortgage origination business at its digital banking arm, Simplii Financial. The guillotine dropped on June 19.

CIBC has quietly pulled the plug on the mortgage origination business at its digital banking arm, Simplii Financial. The guillotine dropped on June 19.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.