There are surprises, and then there are data releases that slap economists harder than a red wine hangover. This was the latter....

There are surprises, and then there are data releases that slap economists harder than a red wine hangover. This was the latter.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Demand for CMHC's multi-unit mortgage insurance skyrocketed 28.7% last year.

Borrowers and lenders have increasingly relied on it to buy, build or refinance multi-unit rental properties.

Unlike uninsured mortgages, CMHC multi-unit financing allows:

* lower down payments

* lower interest expense (lower rates)

* easier debt servicing, thanks to stretched-out amortizations

Take a $15.6 million, 48-unit construction loan under MLI Select, for example. A qualified insured borrower can save ~12...

Demand for CMHC's multi-unit mortgage insurance skyrocketed 28.7% last year.

Borrowers and lenders have increasingly relied on it to buy, build or refinance multi-unit rental properties.

easier debt servicing, thanks to stretched-out amortizations

Take a $15.6 million, 48-unit construction loan under MLI Select, for example. A qualified insured borrower can save ~12% on the monthly payment and buy with $3 million less down, versus a conventional mortgage.

In 2024 alone, CMHC's multi-product helped fund 283,000 housing units. That makes it pivotal to the Carney government’s housing supply dreams.

The challenge is that CMHC is the only game in town for insured multi-unit financing. That's why the price it charges for insurance premiums is so impactful.

And now, those premiums are going up, in some cases, a lot.

Unfortunately—and God bless them—CMHC's specialty is not providing simple, straightforward, and comprehensive explanations of its commercial policy changes. It would be swell if they created a side-by-side before-and-after comparison of each change—you know, to help people understand this stuff. But alas, we ask too much.

What's changing

Starting on July 14:

NEW: CMHC is standardizing the pricing for all multi-unit (MU) insurance products, including MLI Select. Fewer pricing tables to confuse customers are a good thing.

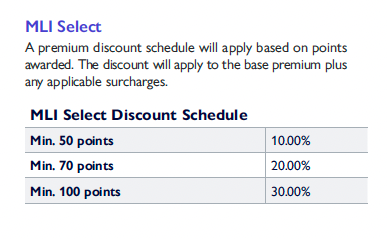

NEW: A new premium discount schedule for MLI Select applications will take effect. The purpose: to lower premiums "based on the level of social outcomes achieved by the borrower, such as affordability, accessibility, or energy efficiency," CMHC says.

Source: CMHC

NEW: Premiums are heading higher for CMHC’s standard ("Market") insurance for retirement homes, student housing, single room occupancy and supportive housing, says Nadeem Keshavjee, President, Founder at GreenBirch Capital.

Fortunately, there are effectively no changes to premiums for CMHC's "Market" insurance for standard rental housing.

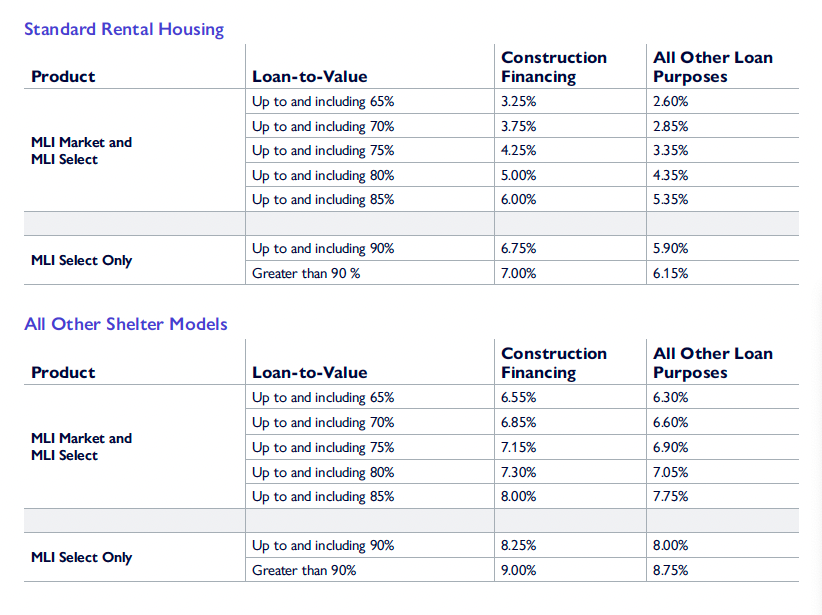

NEW: MLI Select is getting pricier for those pushing the LTV and amortization envelope. Here's the upcoming pricing:

We're talking some hefty price hikes here, my friends. MLI Select premiums prior to the change "ranged from [only] 2.55% to 4.05% regardless of the leverage or amortization," Keshavjee says. (See this)

For non-standard housing (e.g., student rentals at 85% LTV, the purchase premium goes from 6.10% to 7.75%, he adds.

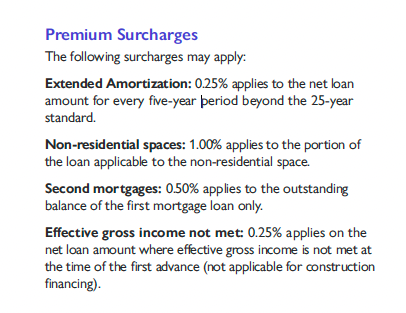

As for current premium surcharges, they'll remain unchanged in all cases. Just note, however, that CMHC never used to levy a premium surcharge for extending MLI Select amortizations beyond 25 years. Now it does. So if you want a 40-year amortization, that's another 75 bps on top of the MLI Select premiums in the above table.

Source: CMHC

Breaking it down

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

Did mortgage shoppers get short-changed this rate cycle?

That's a question the National Bank of Canada (NBC) set out to answer in a new report. Its findings reveal that the prior three BoC cutting cycles delivered "much more relief" to fixed-rate borrowers.

Before we delve into that point, however, here's a peek at how much the BoC's 225 bps of easing lowered bond yields so far....

Did mortgage shoppers get short-changed this rate cycle?

That's a question the National Bank of Canada (NBC) set out to answer in a new report. Its findings reveal that the prior three BoC cutting cycles delivered "much more relief" to fixed-rate borrowers.

Before we delve into that point, however, here's a peek at how much the BoC's 225 bps of easing lowered bond yields so far.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

DLC co-founders Gary Mauris and Chris Kayat, and Wind Mobile co-founder Anthony Lacavera, were part of a consortium that took a controlling stake in WealthONE Bank.

The group dropped $58 million for an almost two-thirds interest in the bank, which the Globe & Mail reports has never made a profit.

Past performance doesn't predict future results, however, especially with the right leadership. These guys above could probably invest in dial-up internet and still turn a profit.

Most likely, this d...

DLC co-founders Gary Mauris and Chris Kayat, and Wind Mobile co-founder Anthony Lacavera, were part of a consortium that took a controlling stake in WealthONE Bank.

The group dropped $58 million for an almost two-thirds interest in the bank, which the Globe & Mail reports has never made a profit.

Past performance doesn't predict future results, however, especially with the right leadership. These guys above could probably invest in dial-up internet and still turn a profit.

Most likely, this deal is the launchpad for transforming WealthONE from a small-time player into an eventual mid-tier rival in Canada's banking market.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.

You don't have access to this post on MortgageLogic.news at the moment, but if you upgrade your account you'll be able to see the whole thing, as well as all the other posts in the archive! Subscribing only takes a few seconds and will give you immediate access.